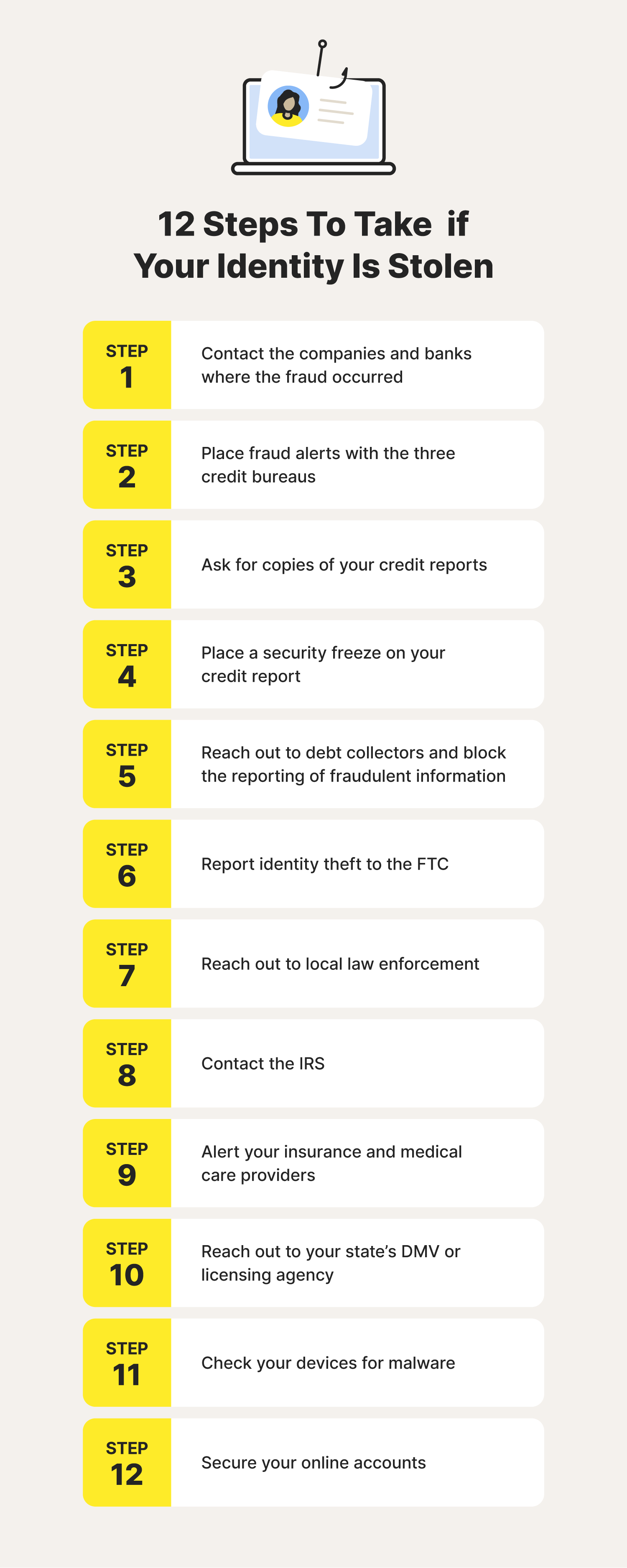

If your identity has been stolen, you’re not alone. In 2022, over 27,000 Americans were affected by identity theft. To help make the identity recovery process easier, we’ve compiled 12 steps to take after identity theft, including:

Let’s get to work!

One of the first things you’ll want to do as the victim of identity theft is assess the damage and contact any company where your identity was used by an identity thief.

How to take action:

- Call the fraud department at the companies and financial institutions where thieves used your personally identifiable information.

- Close or freeze any compromised accounts.

- Ask for copies of any applications or other records related to transactions or accounts connected to the use of your personal information for identity theft.

- Ask that they stop reporting inaccurate information to credit bureaus.

By following these steps, you can help stop the identity thief from using your accounts and start the recovery process immediately.

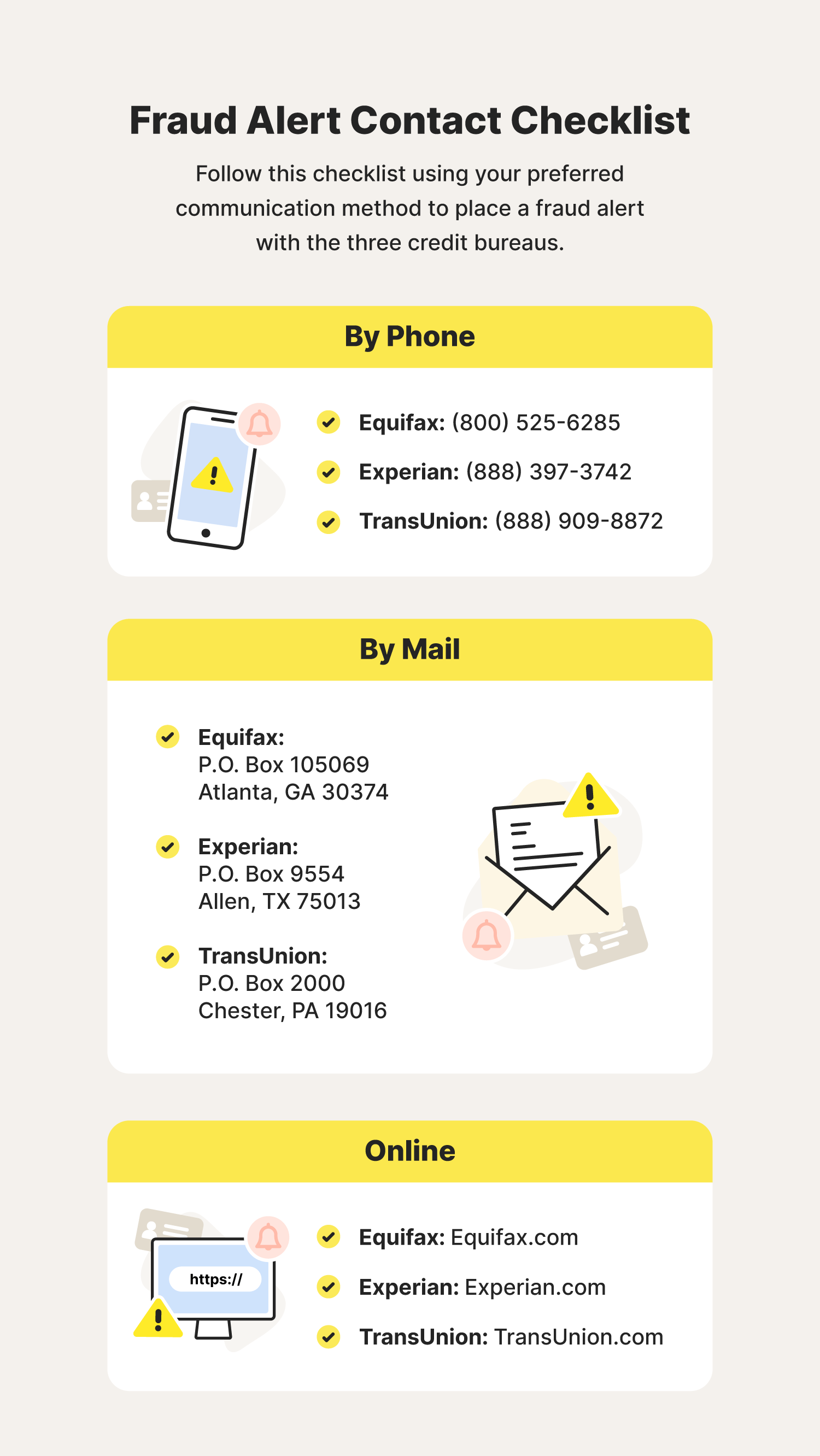

Next, you’ll want to contact at least one of the three major credit bureaus: Equifax, Experian, or TransUnion. Credit bureaus collect information about you, including how you use credit, whether any business has turned your debt over to a collection agency, or if you’ve filed for bankruptcy.

2. Place fraud alerts with the three credit bureaus

The agency you contact is required to contact the other two and share information. But you may want to reach out to each bureau individually to be sure they are on alert that you’ve been a target of identity theft.

How to take action:

A fraud alert will make it more challenging for someone to open new accounts using your identifying information. Once you place a fraud alert, a business must verify your ID before issuing credit to the person requesting it. You may also request an extended fraud alert that lasts for seven years.

You can apply for a fraud alert in all the ways listed below (phone, online, or mail):

| Equifax |

Experian |

TransUnion |

| (800) 525-6285 |

(888) 397-3742 |

(888) 909-8872 |

Equifax

P.O. Box 105069

Atlanta, GA 30374 |

Experian

P.O. Box 9554

Allen, TX 75013 |

TransUnion

P.O. Box 2000

Chester, PA 19016 |

After placing the initial fraud alert, you can request a free copy of your credit report from each credit bureau. It’s important to look at all three reports to help ensure you’re not missing anything important, because each agency’s report may be different.

3. Ask for copies of your credit reports

How to take action:

- Obtain copies of your credit reports from each credit bureau.

- Review the reports carefully for transactions you don’t recognize.

Keep in mind that placing an extended fraud alert allows you to receive two free credit reports from each of the credit bureaus within 12 months after you placed the alert.

If you know your identifying information has been stolen, you may want to freeze your credit report, which will prohibit a credit bureau from releasing any information in your credit report without your express approval.

4. Place a security freeze on your credit report

How to take action:

- Inform the credit bureaus of your situation.

- Place a freeze on your credit report with each credit bureau.

A security freeze prevents prospective creditors from accessing your credit file, providing an extra layer of protection by preventing creditors from approving new credit, loans, or other services in your name without your authorization. You’ll also want to put a self-lock on your Social Security number.

If you’ve been contacted by debt collectors, you’ll want to ask them for relevant information related to debt incurred as a result of identity theft. Additionally, ask the credit bureaus to block any information in your file resulting from identity theft.

For example, an identity thief may make purchases in your name and never pay for them. If you don’t ask the credit bureaus to block this information, it will remain on your credit report and affect your credit score.

How to take action:

- Request information from relevant debt collection agencies.

- Inform the credit bureaus of any fraudulent debt, and ask them to block it from your report.

Under the Fair Credit Reporting Act (FCRA), it is your right to obtain this information, and debt collection agencies must provide your requested information.

While you don’t need to report a stolen credit card to the FTC, you should report identity theft to the FTC right away. The FTC will create a report you can use to prove the identity theft to businesses and financial institutions.

6. Report identity theft to the FTC

How to take action:

- Fill out the identity theft affidavit at IdentityTheft.gov.

- View and follow your recovery plan.

You may also call 877-438-4338 to report identity theft to the FTC.

The FTC says you may also want to alert your local police department. This is especially true if you know the identity thief or have information that could help with a police investigation.

7. Reach out to local law enforcement

How to take action:

- Contact your local law enforcement agency.

- Provide them with your official FTC identity theft report, a government-issued photo ID, proof of your current address, and proof that your identity has been used for identity theft—such as debt collection notices.

- Obtain a copy of your police report.

You can also file an online complaint with the FBI’s Internet Crime Complaint Center to launch an investigation and alert relevant federal, state, local, or international law enforcement.

Another step for recovering from identity theft is contacting the IRS to make sure you aren’t the victim of tax fraud. Someone with a combination of your name, date of birth, and Social Security number could file a tax return in your name, hoping to receive a fraudulent refund.

How to take action:

- Call the IRS Identity Protection Specialized Unit at 800-908-4490, ext. 245.

- Inform them of your situation.

- Follow their instructions.

Be sure to respond to any notices from the IRS that may alert you to fraudulent activity.

While identity theft is more often associated with financial fraud, it can also infiltrate your medical care. Because of this, you’ll want to immediately alert your insurance and medical care providers.

9. Alert your insurance and medical care providers

How to take action:

- Contact your medical care providers and inform them of your situation.

- Obtain copies of your medical records and review them for any suspicious activity.

For example, an identity thief who has your personal information could commit medical identity theft by receiving prescription drugs, having surgery, or visiting an emergency room and leaving you to foot the bill.

An identity thief could use your driver’s license or state ID number to impersonate you. They can use your driver’s license number on a check, during a traffic stop, or to produce a fake license.

10. Reach out to your state’s DMV or licensing agency

How to take action:

- Contact your state’s DMV or licensing agency.

- Ask them to place a flag on your license number.

Informing law enforcement of your lost driver’s license or state ID is important in case an identity thief uses it for criminal identity theft.

In some cases, an identity thief may use malware to infect your devices and steal your personal information. To help ensure nobody is snooping on your device, use antivirus software to scan for malicious software.

11. Check your devices for malware

Not only will installing antivirus software help identify and remove dangerous apps and programs that can be used by identity thieves, but it can help reduce the risk of phishing and other online scams.

How to take action:

Run regular scans to check for malicious software.

From social media to online banking, so much of our information lives on the internet. That's why you want to ensure you’re doing everything in your power to keep your accounts secure. This is especially important if any of them have been compromised by an identity thief.

12. Secure your online accounts

How to take action:

These added layers of security can help keep identity thieves out of your online accounts and away from your private information.

Help safeguard your identity with LifeLock Standard

Even after following the steps for what to do if your identity is stolen, you may still be at risk of identity theft in the future. While nobody can totally prevent identity theft, identity theft protection services like LifeLock Standard can provide you with around-the-clock identity monitoring and access to identity theft restoration experts who can help you if your identity is stolen.

FAQs about what to do if your identity is stolen

Read along to learn the answers to some common questions you may have after learning how to recover from identity theft.

How can you tell if your identity has been stolen?

Before thinking about what to do if someone steals your identity, you might wonder how to tell if your identity has been stolen. Common warning signs of identity theft include:

- Unfamiliar loan and credit card applications in your name

- Calls from collection agencies

- Lost mail

- Unexpected credit score drops

If you notice any of these signs, your identity may have been compromised.

How long can the effects of identity theft last?

The time it takes to recover from identity theft depends on your unique situation, including:

- The number and type of accounts compromised

- The time and effort you put forward to help recover from identity theft

Because of this, it's important that you respond quickly to identity theft to help prevent the thief from doing any additional damage in your name.

How can I protect my identity?

With an understanding of what to do about identity theft, you likely want to know how you can help prevent identity theft in the future. While nobody can completely prevent identity theft, there are steps you can take to reduce the risk, such as:

- Safeguarding your Social Security number

- Monitoring your credit reports

- Keeping your personally identifiable information private

- Prioritizing password security best practices

- Using identity theft protection services

Following these steps can make it more difficult for a thief to steal your identity.